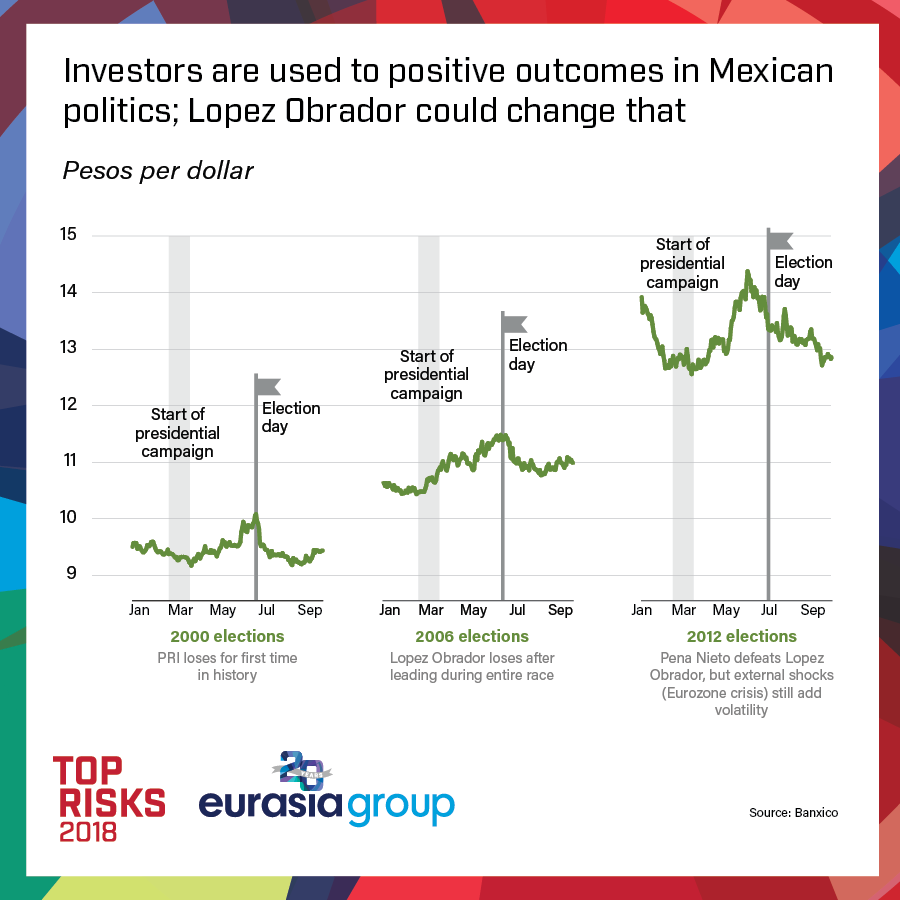

MEXICO WILL HAVE A TOUGH YEAR. Indeed, 2018 will be a defining moment for the country's longer-term outlook, which will depend on the outcome of NAFTA renegotiation and the country's 1 July presidential election. Both carry significant market risks.

First, NAFTA. A successful renegotiation in 2018 is still possible. It's far from certain Trump would act on his threat to initiate withdrawal from the deal; even if he does, this would be a ploy to enhance US leverage in future negotiations rather than an attempt to destroy the agreement. Unfortunately, that's where the good news stops.

Renegotiation of the 23-year-old deal started last August and dominated the second half of the year, with scant results. Increasingly protectionist US proposals have slowed negotiations. Canada, the US, and Mexico share the goal of reaching a deal to revamp the agreement by the end of March, before the presidential campaign begins in Mexico. But successful renegotiation depends on the US softening its stance; Mexico and Canada have few incentives to compromise with the Trump administration, as they know the US business community firmly opposes NAFTA withdrawal.

The NAFTA debate and the country's presidential election are likely to overlap and amplify the risks each presents.

If there is no deal or if Trump initiates a withdrawal process, this would not mark the end of NAFTA, but it would put an end to negotiations. Canada and Mexico would, at least initially, walk away, creating uncertainty over billions of dollars of economic activity in the world's most prosperous region. Though the pain would be shared, the Mexican economy and those who invest in it would suffer disproportionately, given the country's deep reliance on trade with the US.

The NAFTA debate and the country's presidential election are likely to overlap and amplify the risks each presents. Once the presidential campaign starts in March, it will become very hard for government negotiators to agree to meaningful compromises without seeming to bow to the US “hegemonic neighbor.” In addition, the campaign's frontrunner is Andres Manuel Lopez Obrador, known as AMLO, who offers anti-US rhetoric and a statist economic policy platform.

Voter anger at government is running high, thanks to high-profile corruption cases, a deterioration of the security situation, and sluggish economic growth. Public demand for change favors AMLO, and though the ruling Institutional Revolutionary Party (PRI) candidate, Finance Minister Jose Antonio Meade, appeals to independent voters, his association with unpopular President Enrique Pena Nieto will be a burden on his candidacy.

Lopez Obrador is not as radical as some rivals portray him, but he represents a fundamental break with the investor-friendly economic model implemented in Mexico since the 1980s, particularly for the recently enacted opening of the energy sector to private foreign investors. Fiscal constraints and a lack of congressional majorities would limit what he can achieve, but an AMLO presidency, particularly if NAFTA's future remains uncertain, would bring significant market risk to Mexico.