This year will prove another turbulent one for US-China relations, with several irritants that will threaten to derail the thaw the two sides established over the course of 2023.

First, if Vice President William Lai wins Taiwan's presidential election, Beijing will take aggressive military and economic steps to discourage his pro-independence ambitions. Policymakers in Washington will respond with a show of support for Taiwan (please see box in Top Risk #5). Second, China's drive to assert its regional interests will continue to produce close encounters with US military assets in or above the Taiwan Strait and the South China Sea. Third, tech competition between the US and China will continue apace as Washington expands restrictions on China's semiconductor and artificial intelligence industries while Beijing retaliates with further export controls on critical minerals and green technologies (please see Top Risk #7).

Yet we expect the US and China to maintain comparatively stable ties in 2024. There are several reasons why.

While committed to "systemic competition,” President Joe Biden's administration is more immediately determined to put a floor beneath the relationship and preserve the guardrails established by Biden and Chinese President Xi Jinping at the Woodside Summit. Election-year politics in the US will limit cooperation and occasionally dial up hostile rhetoric and actions (please see Top Risk #1). But new diplomatic and military-to-military channels will help manage tensions with Beijing.

Beijing's recent charm offensive—a far cry from the “wolf warrior” diplomacy of Xi's first two terms—will continue, as China's domestic economic challenges and the structural issues underpinning them (please see Top Risk #6) remain defining priorities in 2024 and beyond. The importance of social and economic stability at home and the need to ease the fears of foreign investors and trading partners will continue to override inclinations for a more pugnacious foreign-policy approach. Moreover, given the significant uncertainty—and growing concern—about how Donald Trump might approach US-China relations in a second term, China's leadership has incentives to reinforce engagement while the option is still on the table.

The most important geopolitical relationship in the world is still fundamentally adversarial and marked by mistrust; several flashpoints will exacerbate bilateral tension throughout 2024. But preserving stability is better for both sides this year, neither of which wants to risk major decoupling or conflict. The two countries will carefully manage the relationship's decline as they weather any expected turbulence.

Populist takeover of european politics

A surge in support for far-right and populist parties within many European countries is fueling concern that the centrist consensus that has defined Europe's postwar order could break down in 2024.

In 2023, Geert Wilders and his Freedom Party secured mainstream support for the first time to win the Dutch elections. Robert Fico's left-wing nationalist Smer came back to power in Slovakia. Support for the far-right Alternative for Germany (AfD) surged to record highs. Far-right and far-left parties in France currently have over 50% support combined. Economic headwinds, migratory pressures, some Ukraine war fatigue, and intra-EU discord are kindling fears of a populist sweep at the European Parliament elections in June.

But Europe's center will hold in 2024.

Euroskeptic and populist parties should capture around a quarter of European Parliament seats. An alliance of Europe's center-right parties with far-right and populist parties is politically unlikely. Even if their politics align, they will not account for a sizable majority in the European Parliament. Therefore, the traditional European coalition—comprising the center-right, social democrats, liberals, and Greens—will maintain power in the EU's legislature, and the European Commission (the bloc's executive) will be chosen by consensus among centrist candidates.

Hungarian Prime Minister Viktor Orban will continue obstructing EU decision-making, but centrist governments in the majority of member states will manage to find workarounds. Moreover, Orban will no longer have the support of his crucial former allies in Warsaw after Polish voters replaced a xenophobic right-wing government with an EU-friendly centrist one in 2023. Despite pushback from Hungary and other headwinds, financial support for Ukraine is likely to be maintained near current levels this year. Even in countries led by antiestablishment parties, such as Italian Prime Minister Giorgia Meloni's Brothers of Italy, decision-making will remain overwhelmingly pragmatic—even centrist.

Populists and right-wingers will continue to make gains and strike fear into the European political establishment. But limited setbacks for mainstream parties in European Parliament, national, and local elections will neither upend the European political order nor fundamentally derail revamped EU ambitions following the twin crises of the Covid-19 pandemic and the Ukraine war.

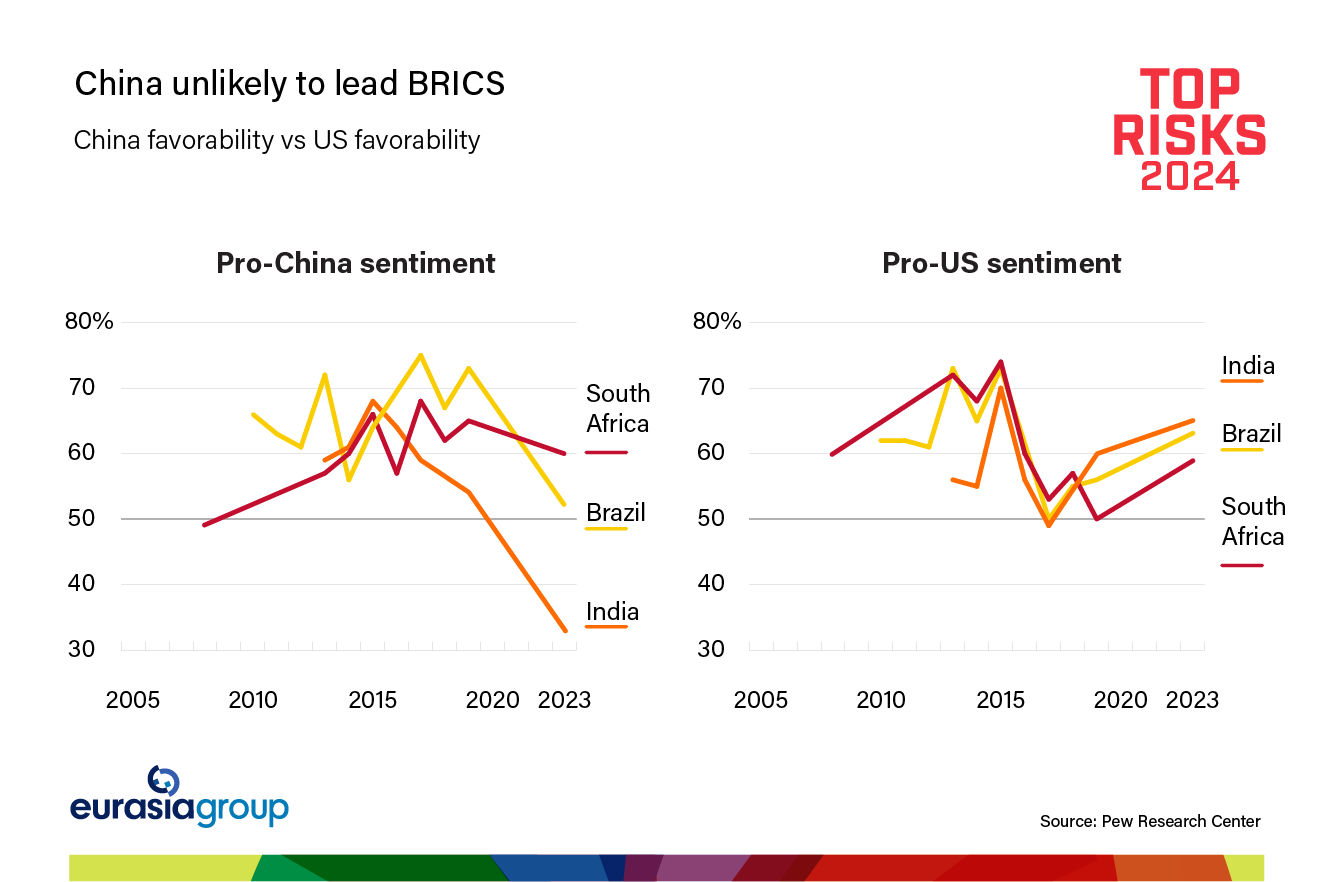

brics vs. g7

On 1 January, the BRICS welcomed new members Saudi Arabia, Iran, Egypt, the United Arab Emirates, and Ethiopia. Some have argued that this expanded BRICS will become an anti-US counterweight to the G7 and the West. This view also holds that China will co-opt the organization, and through it, expand its influence over the Global South.

We disagree.

The expanded BRICS, like the original organization, will be a weak group, with much less institutional coherence than the G7. The group's original members—China, India, Russia, South Africa, and Brazil—have little in common beyond a shared desire to boost their status on the global stage. They also have dramatically different political and economic systems. The addition of new members will make consensus—a requirement for the group to take any action—even harder to reach than it already is. The expanded BRICS now includes two pairs of countries that are longtime rivals: China and India plus Saudi Arabia and Iran.

China will have important influence in the BRICS, to be sure, but its attempt to co-opt the group won't work. India is a critical member—especially and increasingly as a leader of the Global South—and will oppose most initiatives that strengthen Chinese clout. Also, most BRICS countries seek good relations with both the US and China and don't want to jeopardize their existing (and in some cases growing) diplomatic and commercial ties with the G7. Therefore, they will place limits on Chinese sway.

The BRICS will not emerge as a China-led rival to the G7 this year—or anytime soon.

Sign up now for GZERO Daily, the newsletter for anyone interested in global politics, published by GZERO Media.

We have updated our Privacy Policy and Terms of Use for Eurasia Group and its affiliates to clarify the types of data we collect, how we collect it, how we use data and with whom we share data. This website uses cookies. By using our website you consent to our Terms and Conditions and Privacy Policy, including the transfer of your personal data to the United States from your country of residence (if different), and our use of cookies as described in our Cookie Policy.

.png)

.png)