The global inflation shock that began in 2021 will continue to exert a powerful economic and political drag in 2024. High interest rates caused by stubborn inflation will slow growth around the world. With macroeconomic policy buffers largely exhausted, governments will have limited scope to stimulate growth or respond to shocks, heightening the risk of financial stress, social unrest, and political instability.

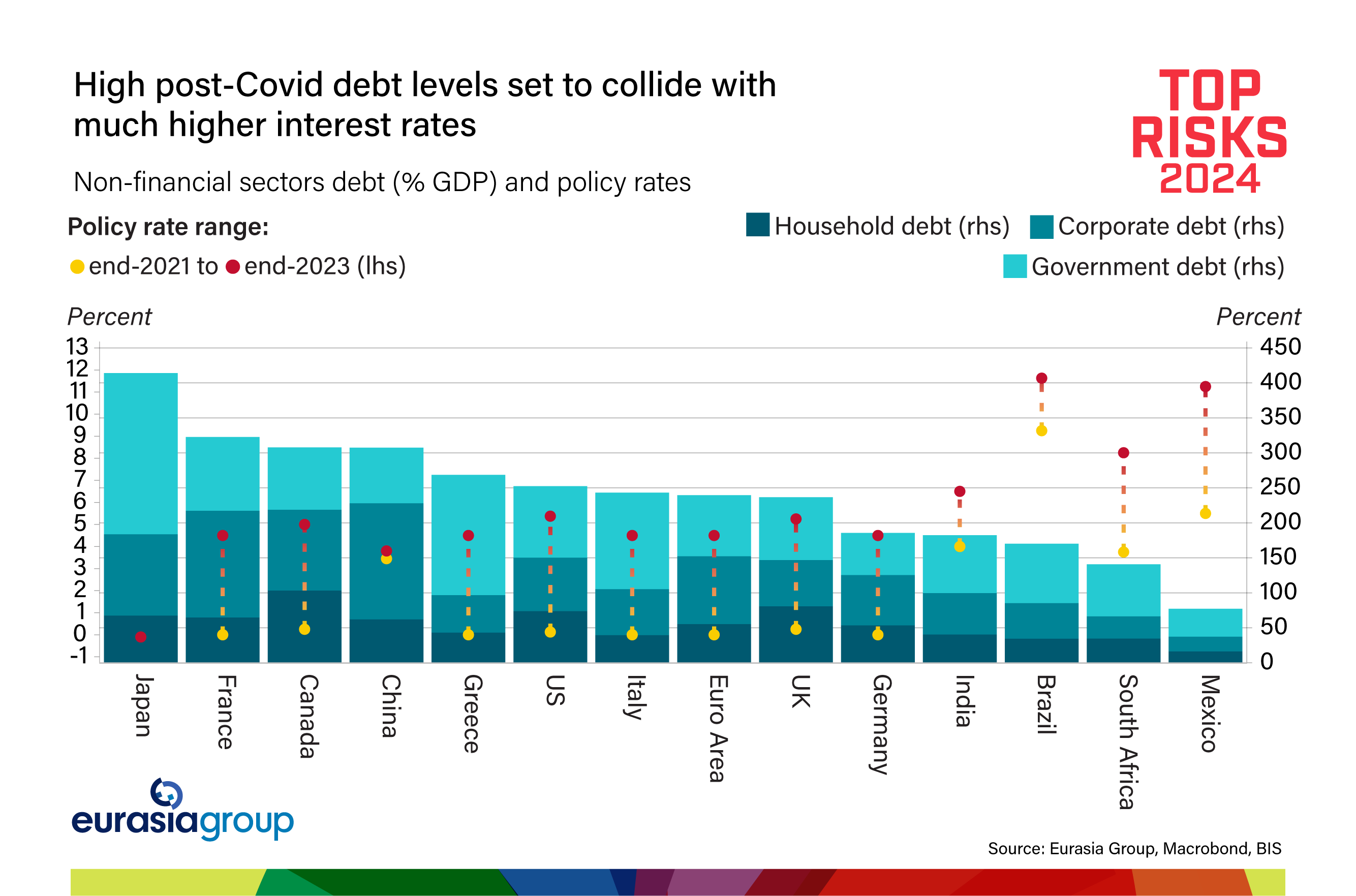

While 2023 saw a significant deceleration in inflation and the end of the monetary tightening cycle, global interest rates remain highly restrictive. Despite expectations of a substantial easing in monetary policy, persistently above-target inflation will lead central banks to keep interest rates high in 2024. Their efforts to cool inflation without sparking a recession will be hindered by inflationary pressures over which they will have no control: The ongoing war in Ukraine will keep commodity prices high and volatile (please see Top Risk #3), the ongoing war in the Middle East will raise freight costs and disrupt global supply chains (please see Top Risk #2), and El Nino will threaten food prices (please see Top Risk #9). Moreover, political and geopolitical calculations by major oil producers will keep oil prices—which usually act as a countercyclical stabilizer in times of low growth—relatively elevated, while industrial policies aimed at boosting national security and supply chain resilience will lead to growing geoeconomic fragmentation and higher prices.

Sticky inflation and tight financial conditions will weaken global demand and exacerbate economic insecurity. Faced with persistent inflationary pressures and rising debt-servicing costs, households and firms will retrench. Fiscal policymakers—especially those under pressure from market stress—will be reluctant to step in, instead focusing on reducing public spending after several years of pandemic-related deficits. Chinese growth, once a safety net during global downturns, will remain too weak to fill the gap (please see Top Risk #6). As a result, much of the world will experience subdued growth, and many countries will dip into recession.

With policy space already diminished by the pandemic response, “de-risking” efforts, the energy transition, the Russia-Ukraine war, and soaring interest costs, any additional negative supply shocks would prompt central banks to tighten rather than ease monetary policy to rein in inflation expectations, depressing growth further. At the same time, widening political divisions within many countries and geopolitical tensions among them will reduce the scope for domestic crisis response and global policy coordination.

These economic headwinds will deepen voter discontent in a year when two-thirds of adults in the democratic world will go to the polls, hurting weak incumbents and boosting populist challengers. In the United States, despite improving economic fundamentals, negative perceptions of the economy will be a drag on President Joe Biden's reelection bid, while in the United Kingdom, the Conservative Party is set to be voted out on the back of weak growth. In South Africa, meanwhile, the ruling African National Congress faces the prospect of losing its parliamentary majority for the first time since the end of apartheid thanks to a chronically weak economy.

In countries without scheduled elections in 2024, a shrinking economic pie will cause fiercer fights over the distribution of scarce resources, leading to social unrest and political instability. Those with the lowest growth rates, highest debt levels, and most divisive politics will be most vulnerable. Some governments will be under intense pressure to enact fiscally unsustainable populist or heterodox policies, in turn exacerbating their inflation and debt problems. In Nigeria, popular discontent will undermine the government's ability to advance reform priorities such as removing fuel subsidies and introducing more flexibility in the foreign exchange market. In Brazil, a slowing economy and faltering government approval ratings will prompt President Luiz Inacio Lula da Silva to weaken the country's fiscal framework. And having just been elected to implement radical changes, Argentina's President Javier Milei will struggle to address deep economic imbalances amid mounting social backlash.

Heightened economic, financial, and political strain will provoke debt distress in emerging and frontier economies with the least capacity to respond. In addition to those already undergoing debt restructurings—Zambia, Ghana, Sri Lanka—borrowers such as Pakistan and Egypt could be forced to default on their debts. The largest creditor nations, most notably China, will be reluctant to provide meaningful multilateral debt relief. Developed markets with high debt levels such as Italy and Canada, meanwhile, will also face fiscal and financial strain in this environment. Although they will have enough economic and political capacity to address these challenges, rising debt service costs will crowd out spending on public goods.

While financial markets proved resilient in 2023, persistently high interest rates, tepid growth, and exhausted buffers will heighten the risk that something breaks. Last year's bond market volatility and the banking crisis triggered by the collapse of Silicon Valley Bank could return, or other interest rate-sensitive markets such as real estate, corporate debt, and insurance could face real stress. With growth subdued and policy set to remain tight, further accidents are bound to happen.

Sign up now for GZERO Daily, the newsletter for anyone interested in global politics, published by GZERO Media.

We have updated our Privacy Policy and Terms of Use for Eurasia Group and its affiliates to clarify the types of data we collect, how we collect it, how we use data and with whom we share data. This website uses cookies. By using our website you consent to our Terms and Conditions and Privacy Policy, including the transfer of your personal data to the United States from your country of residence (if different), and our use of cookies as described in our Cookie Policy.