Any green shoots in the Chinese economy will only raise false hopes of a recovery as economic constraints and political dynamics prevent a durable growth rebound. Consolidation of power at the top (Eurasia Group's Top Risk #2 for 2023) has snuffed out policy debate and animal spirits just as China's past growth engines have been exhausted, and there is little the government will do to reverse either trend. Beijing's failure to address the country's sputtering growth model, financial fragilities, insufficient demand, and crisis of confidence will expose gaps in the legitimacy of the Chinese Communist Party (CPP) and increase the risk of social instability.

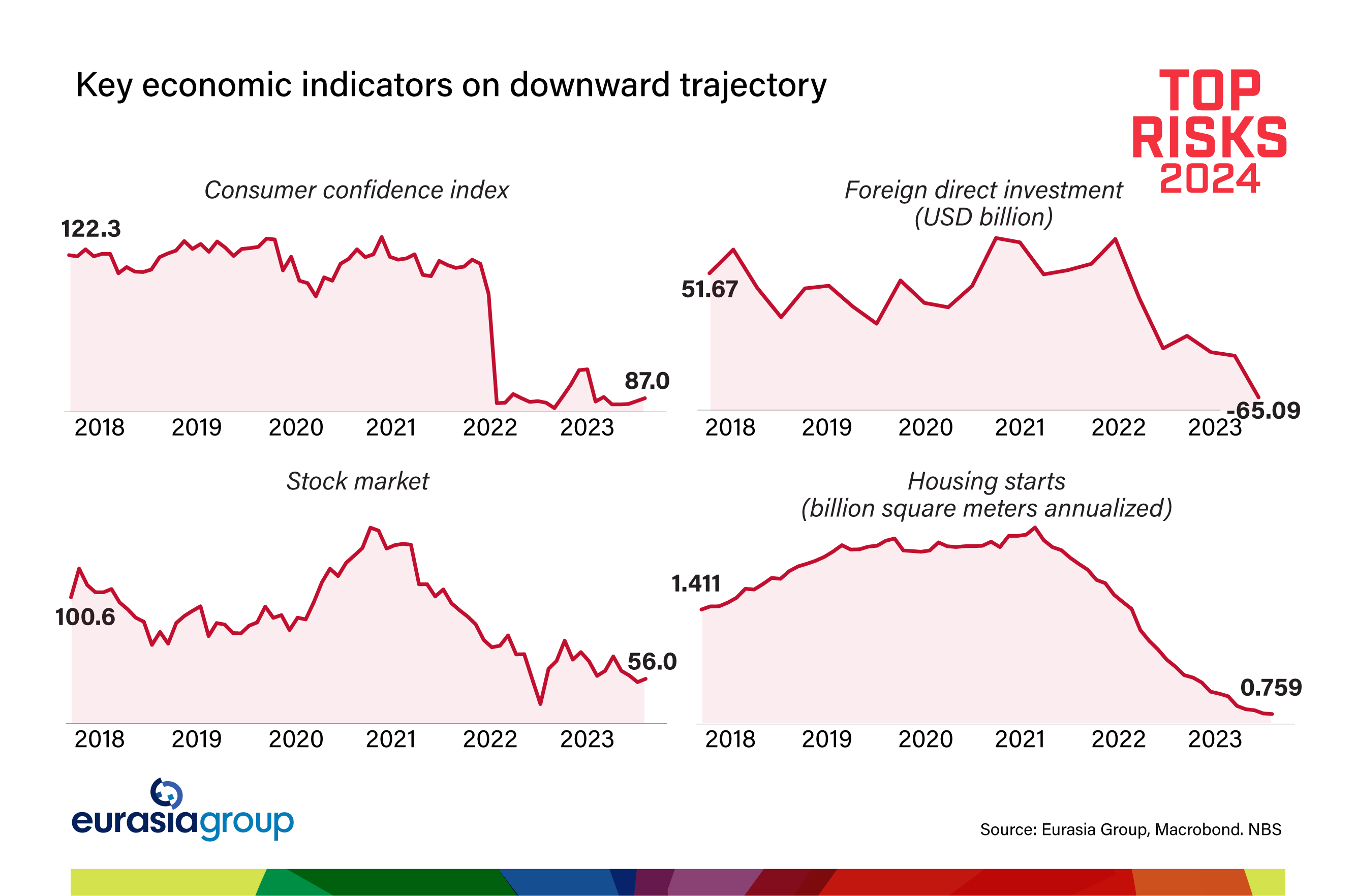

We've already seen warning signs of deepening malaise emerge in 2023, from the exit of foreign investors and Moody's outlook downgrades to stalled property purchases and a stock market slump. This year, appetite to re-invest in the country will continue to be dampened by vague and conflicting policy signals, growing concerns about geopolitical risk, and the CCP's ongoing regulatory crackdowns.

The persistence of constraints such as unfavorable demographics, eroding labor cost advantages, high indebtedness (particularly at the local level), Western “de-risking” efforts, and continued reliance on state investment for growth will further diminish hopes of a resurgent Chinese economy. While Beijing will try to restore confidence and prop up demand by throwing more money at the problem—building yet more infrastructure to meet its likely 5% growth target (again) for 2024—its efforts will have limited impact in the absence of a true shift toward bold reform.

Four additional economic factors will impede a recovery in 2024:

1)Fading zero-Covid rebound. The tailwind from last year's reopening will disappear as slowing income growth, higher unemployment, local government fiscal consolidation, falling property prices, and cascading defaults weigh on confidence and consumption.

2)Real estate weakness. Previously a pillar of China's economy, the real estate sector won't provide a much hoped-for boost despite recent stabilization efforts, with new construction remaining anemic owing to weak homebuyer demand and slumping land purchases by cash-strapped property developers over the past two years.

3)Low external demand. International demand for Chinese exports, especially from the US and Europe, will prove less resilient than in 2023, constrained by high interest rates and slow global growth (please see Top Risk #8).

4)Government economic response. Beijing's whack-a-mole approach to emerging episodes of financial stress such as developer defaults and bank collapses (as opposed to larger-scale, more preemptive reform) will sap confidence and test the government's already-stretched administrative capacity.

Then there's politics. President Xi Jinping's concentration of power and prioritization of security over growth will not only weigh on consumer, business, and investor confidence, but it will also make the regime slower to respond to rising economic and financial vulnerabilities. This doesn't mean that China faces an imminent crisis. Rather, these conditions will entrench the country's economic malaise and expose cracks in the CCP's veneer of competence and legitimacy.

Absent an unlikely loosening of Xi's grip or a radical pivot toward large-scale consumer stimulus and structural reform that restore confidence and reignite growth, China's economy will underperform throughout 2024. While the CCP's rule is stable, there remains a longer-term risk that Beijing will react too slowly to warning signs of financial contagion and social unrest, increasing the chances that the government could one day lose control of both.

Sign up now for GZERO Daily, the newsletter for anyone interested in global politics, published by GZERO Media.

We have updated our Privacy Policy and Terms of Use for Eurasia Group and its affiliates to clarify the types of data we collect, how we collect it, how we use data and with whom we share data. This website uses cookies. By using our website you consent to our Terms and Conditions and Privacy Policy, including the transfer of your personal data to the United States from your country of residence (if different), and our use of cookies as described in our Cookie Policy.