Short-term vulnerability, long-term opportunity

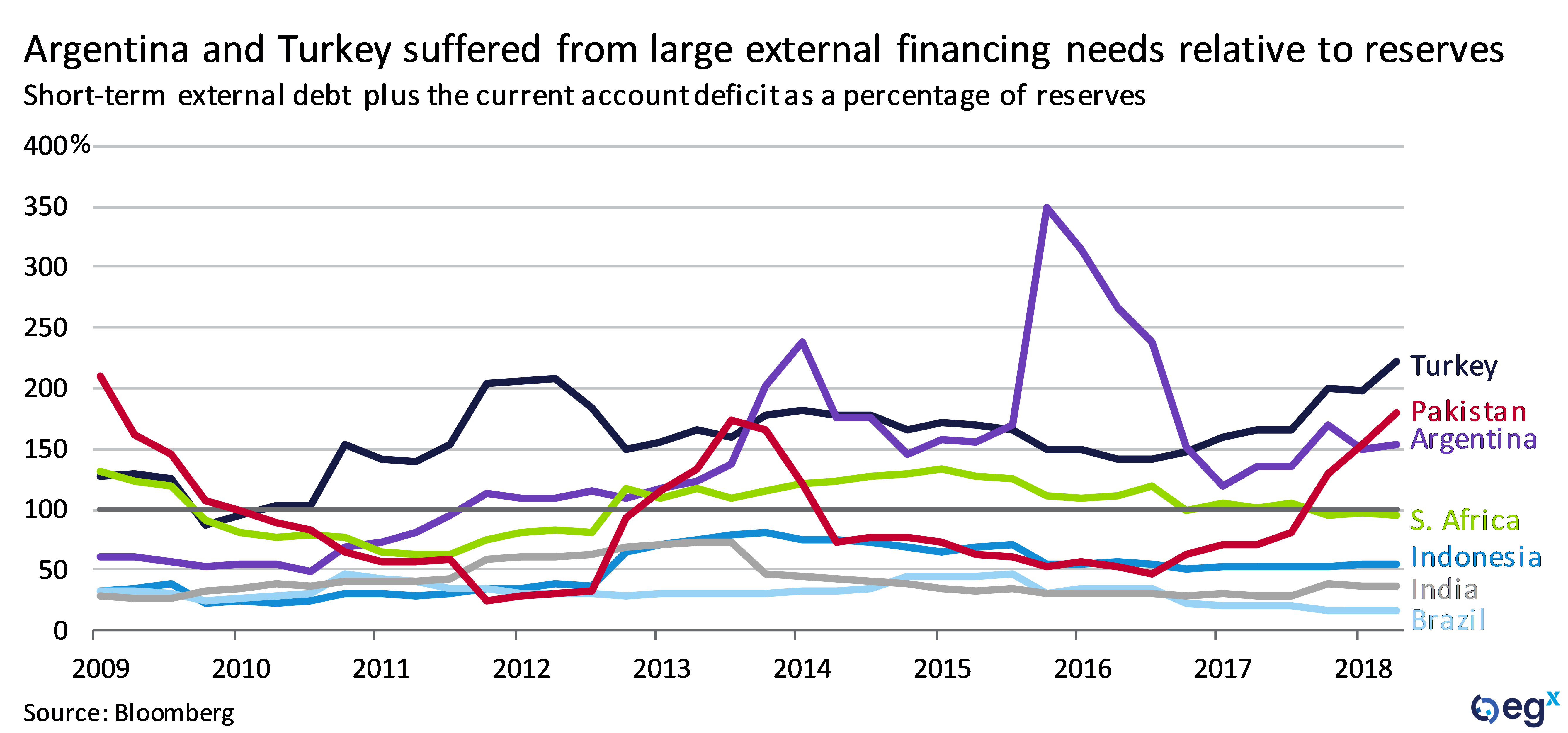

For much of the past year, financial risks and trade concerns have dominated the emerging market (EM) financial headlines. Countries such as Argentina and Turkey were major underperformers due to their foreign currency liabilities, short-term debts and questionable external financing capacity.

Conversely, Asian EMs were left largely unscathed despite their connections to China, and by extension the US “trade war.”

Short-term pain

Short-term pain

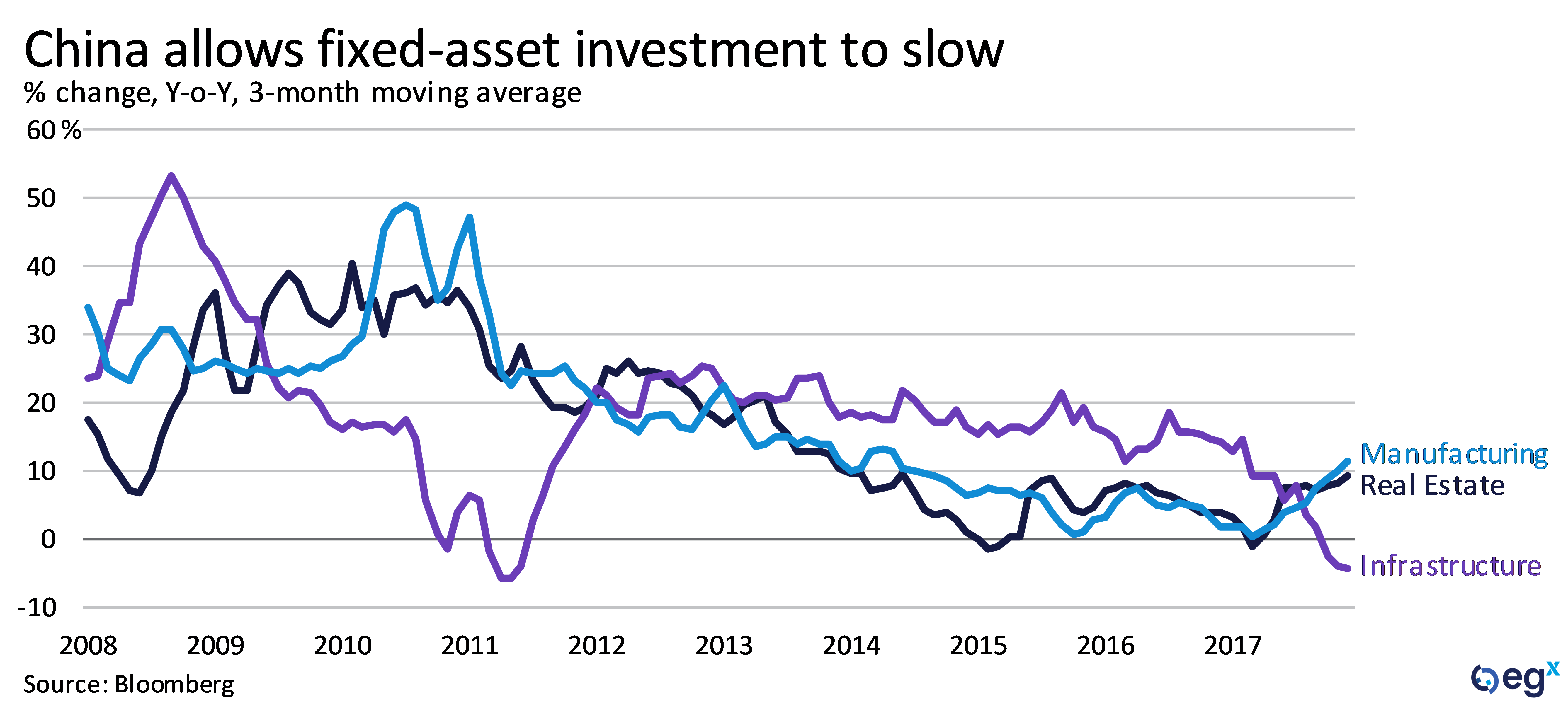

Pressure on the Southeast Asian economies continues to mount, however, largely due to increased strain on the Chinese economy. Policymakers in China are attempting to navigate three main obstacles: the ongoing trade dispute with the US, the need to reduce risks within the financial sector, and a broader shift to a less investment-driven economy.

China now accounts for roughly 35% of annual global GDP growth. Although growth should remain north of 6%, marginal decreases in the growth rate generate negative reverberations globally, and outsized repercussions for countries highly reliant on Chinese growth. In an environment where EM risks are shifting from financial risks to real economic risks—those that are felt via trade and foreign direct investment channels, particularly when the nucleus is China—Asian EMs are squarely in the firing line.

Long-term gain?

Long-term gain?

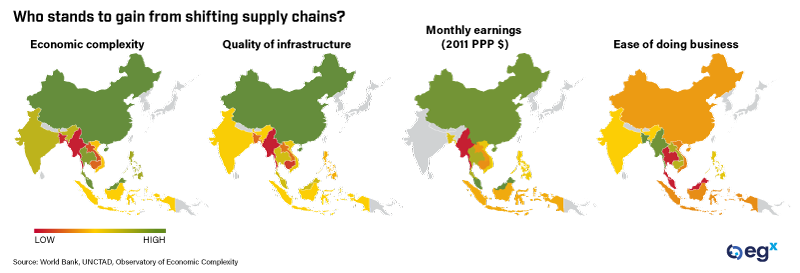

These challenges portend that Southeast Asian EMs could be in for some pain, however the combination of Chinese economic rebalancing and trade-war-related supply chain disruptions could create opportunities for the region.

First, Beijing's focus on boosting domestic consumption over fixed asset investments means that Chinese demand for foreign goods should increase over time.

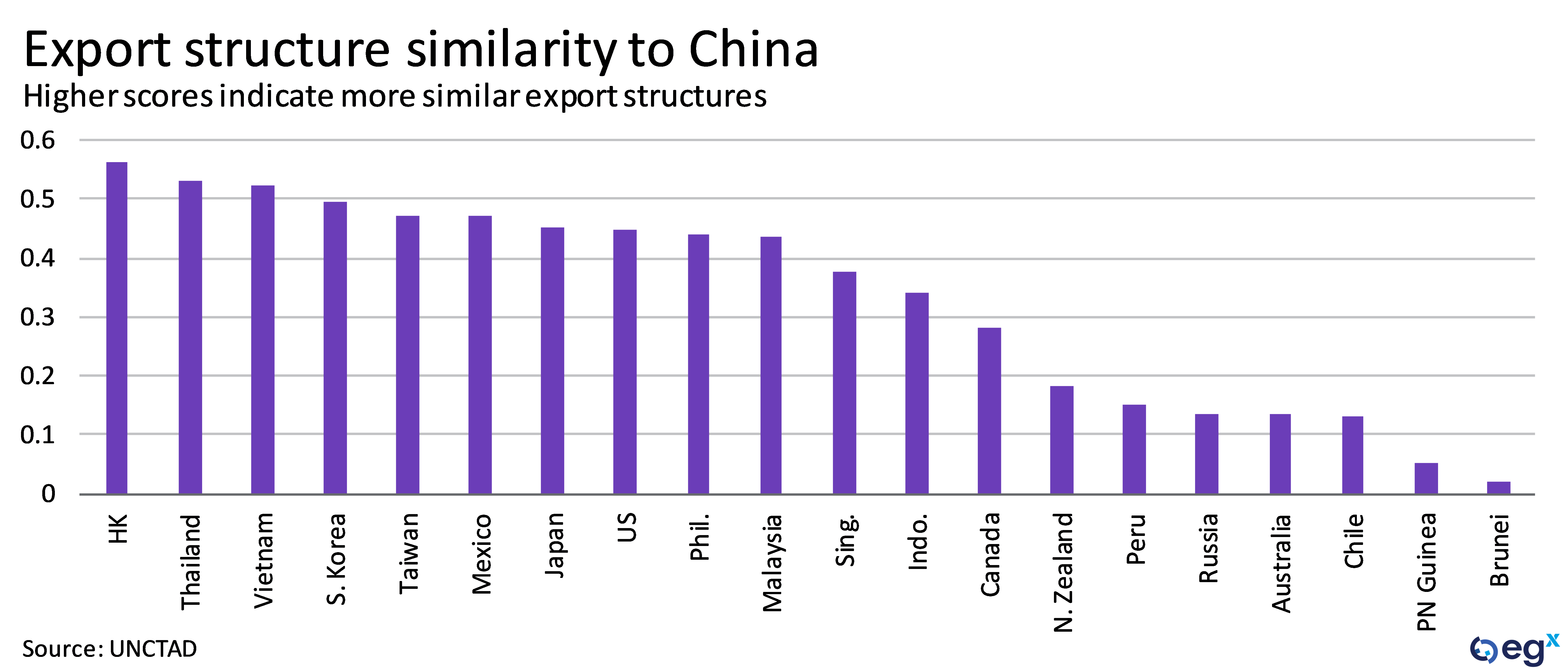

China's ascent up the value-added production ladder will make room for other countries to fill the void in lower value-added export production. The transition toward a more consumption-oriented economy also will create opportunities for exporters who can service Chinese final demand for goods and services.

Finally, US efforts to remove China from global supply chains through tariffs, export controls, and limitations on technology transfer could open the door for countries with similar productive and logistical capacity that are less geopolitically threatening to the US.

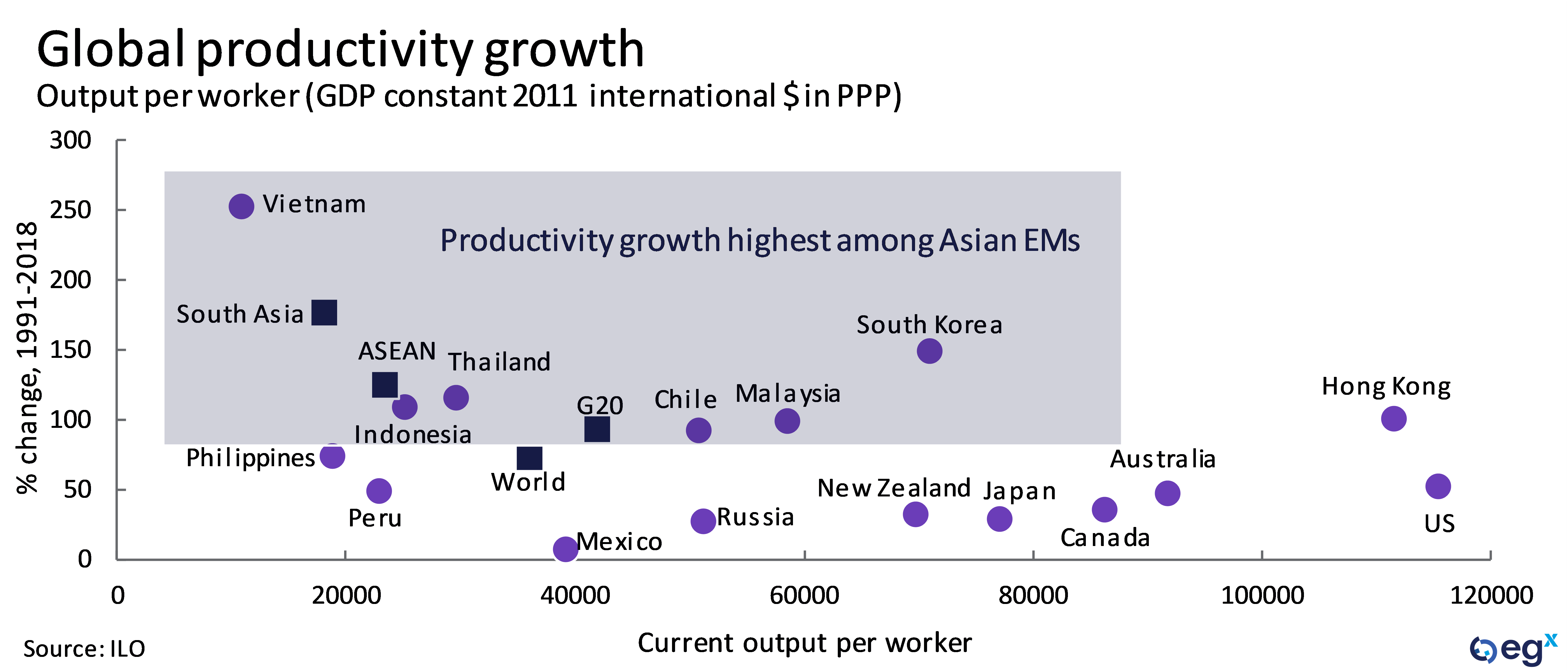

This trend could create opportunities for economies such as Vietnam, Indonesia, Malaysia, and Thailand that offer access to diversified economies with robust infrastructure, relatively-lower wages, and supportive business climates.